Pandora is feeling mighty bullish.

Last night, the US streaming platform announced its intention to acquire key assets from on-demand music service Rdio – which, it transpires, is about to file for bankruptcy in the States.

Pandora CEO Brian McAndrews (pictured, main) and CFO Mike Herring (pictured, inset) addressed investors after the $75m buyout was announced.

Their comments made for fighting talk – in stark contrast to Pandora’s earnings call last month, which carried a tinge of near-defensiveness as the firm admitted that it had lost over a million listeners in Q3.

Now, though, Pandora is beating its chest again – with McAndrews and Herring explaining how the company expects to dominate global music streaming in the coming years and defeat rivals such as Spotify.

Here’s what you need to know in a post-Rdio world…

1) PANDORA FANCIES ITS CHANCES AGAINST SPOTIFY – WHOSE BUSINESS MODEL IT SUSPECTS IS BROKEN

To get a handle on Pandora’s chances of overcoming Spotify in the global on-demand music streaming race, first you need to appreciate where its business is right now.

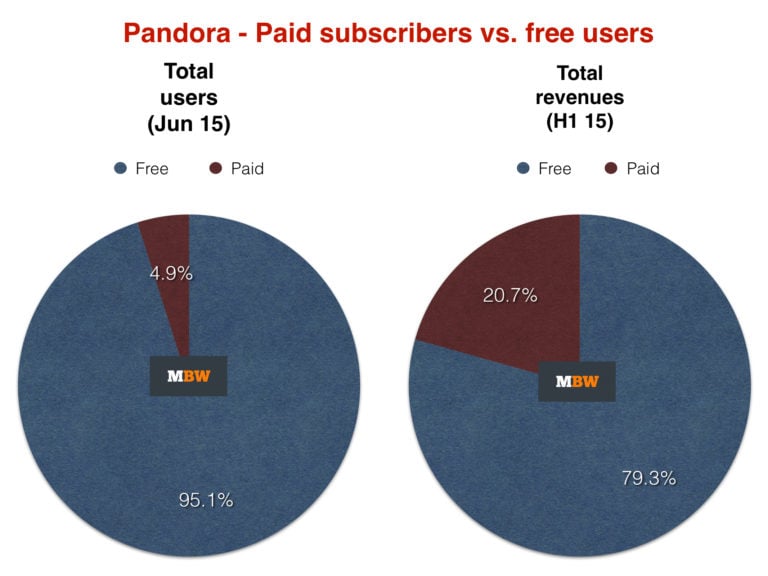

As analysed by MBW earlier this year, Pandora has found it tough to grow its existing subscription tier, Pandora One – which contributes around 20% of its revenue, but appeals to less than 5% of its 78m listeners.

Currently, Pandora is essentially a ‘lean-back’, or non-interactive, streaming service. This is why people have loosely called it ‘digital radio’ – it chooses songs for you, peppered (on its dominant free tier) with ads.

Although Pandora often struggles to post a business-wide profit, CFO Mike Herring claims that the core ad-funded streaming service (minus, presumably, marketing and other customer acquisition costs) is profitable.

By launching a paid-for tier on top of this solid footing, he says, Pandora is in a far healthier state than its rivals. Especially the big green one.

(Which we’ve taken to calling a ‘Swedish service’, but whose fiscal holding company is actually not in Stockholm but in Luxembourg… where it files its annual accounts.)

Pandora’s big challenge here is that the licensing costs for interactive streaming services vs. non-interactive streaming services are typically much higher.

“The on-demand business that exist today – and the licensing that’s available – is a low-margin business, certainly lower margin from a contribution perspective than the ad-supported business,” Herring told investors last night in a blatant criticism of Spotify’s fiscal footing.

“One of the reasons why those business struggle is that they have to spend a lot of money trying to acquire customers and convince them to convert. When you’re spending all these dollars in marketing and you’re doing deals with [telco] carriers and such to try to build a pool of people to try and convert [to premium], it’s really hard to try and make up for that with a low-margin [business].

“PANDORA’S BUSINESS MODEL HAS A MUCH HIGHER PROBABILITY OF SUCCESS THAN ONE THAT RELIES PURELY ON AGGREGATING PEOPLE FOR CONVERSION TO PREMIUM.”

“The volume necessary to make up [that gap] is huge – and is yet to be proven to even possible on an independent basis.

“The advantage Pandora brings is we have a fantastic, non-interactive ad-supported business that has a significant positive contribution margin itself. Our ability to attract tens of millions of users [to ad-funded], a huge pool of people happy to listen to our service, is actually a contribution margin-positive, profitable business.

“We don’t need to make up customer acquisition costs for the upsell into subscription business [for Pandora] to make financial sense. We have the unique position of looking at subscription… not as [a] core business that we need to justify customer acquisition costs.

“If you can take a profitable, ad-supported, free-to-consumer business and layer onto it additional, profitable revenue streams from paid-for listening and subscriptions… and add onto that very profitable ticketing, event promotion and sponsorship business through our [$450m] Ticketfly acquisition… we’re layering together numerous businesses all of which are all contributing to the bottom line.

“That’s a business model with a much higher probability of success than one that relies purely on aggregating people for conversion [into premium].”

As for Apple Music, Pandora’s argument sounds remarkably like Spotify’s…

“We are a music company,” said Brian McAndrews last night. “A singular focus on music gives us clarity of mission and aligns our ambitions with the music industry… Because music is our focus, we will work harder and be more innovative. As a result, the industry has no more dependable ally than Pandora.”

2) PANDORA IS SCARED OF WHAT THE US COPYRIGHT ROYALTY BOARD MIGHT DECIDE IN A FEW WEEKS

The US licensing rate setting procedure is anything but simple.

The main thing you need to know is that, as we move towards Christmas, online ‘radio’ services face a nerve-wracking process.

The Copyright Royalty Board, made up of three judges, has a big decision to make.

Pandora currently pays out an average $0.0014 per ad-funded stream and $0.0024 per premium stream to SoundExchange – which is then paid to artists and labels.

Alongside the likes of other ‘web-casters’ such as Sirius XM and iHeartRadio, Pandora is lobbying the CRB to bring down its current per-stream payout, while SoundExchange wants to double it to $0.0025.

The conclusive new rate, which will only affect recorded music royalty rates, will be announced before the end of this year, and affect rates from 2016-2022.

Herring told investors last night: “We’ve thought carefully and acted deliberately regarding our strategy, including the timing of Rdio and Ticketfly in advance of the CRB outcome.

“IT WAS OUR ANALYSIS THAT IF THE CRB ANALYSIS IS UNFAVOURABLE… OUR AD-SUPPORTED LINE OF BUSINESS WILL OBVIOUSLY DECREASE.”

“To be speak to this directly, it was our analysis that if the CRB [decision] is unfavourable, the contribution margins we can expect from our ad-supported line of business will obviously decrease.

“In this scenario, having other revenue streams to focus on such as subscription businesses and live events promotion gains importance.

“On the other hand, if the rates are reasonable, our ad-supported business will provide continued investment dollars and we will have more options to invest those dollars.”

A bit of maths is crucial to get a handle on this. In Pandora’s last quarter, its ‘content acquisition costs’ – ie. payments to labels and publishers – reached $211.3m. Total revenues stood at $311.6m.

That means licensing fees cost Pandora 68% of its income.

Across the first nine months of 2015, with revenues at $827.9m and royalty payouts at $467.4m, that percentage reduces to 56.5%.

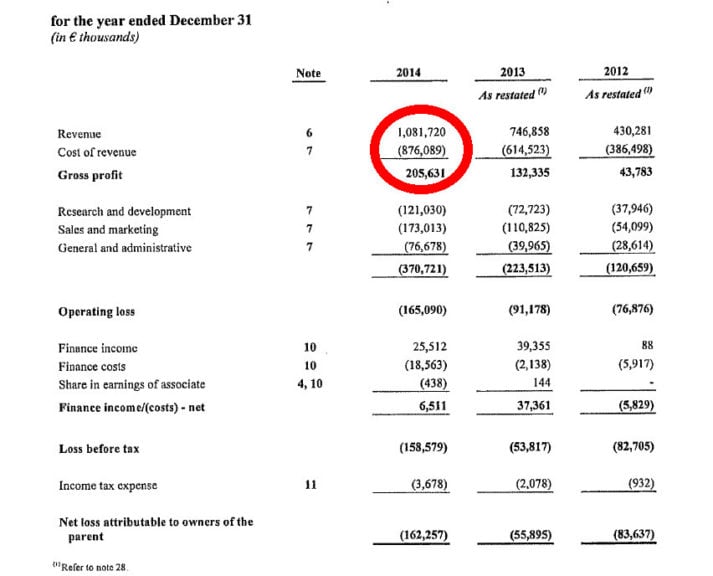

These percentages are high for Pandora, which is more used to seeing 40% – 50% of its income paid out to labels and publishers, but they’re still significantly smaller than Spotify, for example, whose ‘cost of revenue’ (mainly industry royalty payments) swallowed up 81.5% of its €1.08bn total revenue last year (see table below).

That’s before tax, marketing and administration expenses.

(As for how Deezer compares, if you don’t want to openly weep at your desk today, you’re probably better off not asking.)

3) PANDORA NEEDS NEW LICENSES TO LAUNCH ITS ON-DEMAND SERVICE…

In the wake of the Sony/ATV multi-year licensing deal with Pandora the other week, MBW speculated:

“Martin Bandier (pictured inset) may well have permitted Pandora the opportunity to play with some more rights – offline temporary downloads, perhaps, or on-demand elements, or maybe just lyric additions – that ASCAP and BMI don’t have in their jurisdiction.”

That statement now looks accurate, but timid.

Pandora is already using its Sony/ATV direct deal as a precedent for the kind of industry licensing it needs to get done before it launches its an on-demand streaming service – a launch currently pencilled in for late 2016, according to Brian McAndrews.

Forget the CRB: Pandora’s licensing history with publishers – whose income it’s regularly beaten up by battling their ASCAP and BMI in the US Rate Courts – is fraught with bad blood.

“THERE IS NO GUARANTEE THAT ALL POTENTIAL MUSIC PARTNERS WILL WANT TO JOIN US. BUT WE ARE AGGRESSIVELY MOVING FULL STEAM AHEAD.”

At the moment, Pandora pays out around just 4% of its annual revenue to songwriters and publishers (a figure which will total approx $40m this year).

MBW understands Pandora is in licensing discussions with 10-15 publishers as you read this, negotiating direct deals – like Sony/ATV”s – that allow for a higher per-stream rate… but enable Pandora to offer users more interactive experience.

“Unlocking the full global potential of our service…. requires securing agreements with labels and publishers and that is exactly the path we are on,” said McAndrews.

“As we find win-win agreements as we did with Sony/ATV, we believe Pandora is uniquely well suited to help our music business partners achieve their own business objectives”

One further comment from McAndrews might just alarm music industry rights-holders:

“In terms of timing, we are engaged in productive conversation but expect this new approach will take some time to fully materialise… There is no guarantee that all potential partners will want to join us. But we are aggressively moving full steam ahead, optimistic about what our evolving approach will do for Pandora and our music partners.”

Another streaming service which took this approach was Amazon Prime Music. It launched without being licensed by Universal Music Group. Eventually, UMG came on board.

4) … BUT PANDORA’S NOT GETTING RDIO’S LICENSES. OR ITS BOSS. OR, IT APPEARS, ITS USERS.

So what’s Pandora buying from Rdio, and why?

According to CFO Mike Herring, the deal is expected to go through in Q1 next year – at which point Pandora will become the new owner of Rdio’s technology and a handful of staff.

(Those staff won’t include Rdio CEO Anthony Bay: he’s staying on to wind-down the failed business, according to McAndrews.)

Another thing Pandora won’t get as part of its purchase are a set of ready-made licenses for a fully interactive global streaming service.

As Herring explained: “The licensing deals are not transferable. That’s normal.. We will not be operating the business at this time, so we don’t need [the licenses].

“We’ll be concentrating on getting them as we roll out [Pandora’s own on-demand] product.”

“RDIO’S BUSINESS WAS CHALLENGED AND FINANCIALLY WOULD HAVE BEEN A DRAIN.”

McAndrews further explained why Pandora wasn’t taking on Rdio’s operating business, and – when asked directly – appeared to suggest that Pandora would notinherit Rdio’s subscriber base, which is believed to number between 500k and 1m in the US.

“We will be building our own new service with the technology, assets and people we will be [acquiring],” he said. “In that sense, the data from the past business is not particularly relevant to us.

“We think the real strength we bring is all the data we bring with our current business. That’s the strength we’re going to build off with our own upper tier offerings.

“We’ve been successful with Pandora One and we think we can go significantly beyond that.”

So why didn’t Pandora decide to take on the whole of the Rdio business and buy the entire operation?

“The business was challenged and financially would have been a drain, and also would have been a drain of resources,” said McAndrews.

“We’d much rather focus on building our own business than [operating] one we didn’t intend to continue.”

He added: “They had a really good on-demand product, but didn’t have the ability either financially or in their core business to attract enough people… From the beginning we’ll have a base to built a superior product.”

5) PANDORA’S VISION IS PREDICATED ON GLOBAL GROWTH – AND A CLOSER RELATIONSHIP WITH THE MUSIC BUSINESS

Will the music business’s biggest players forgive Pandora’s past sins?

Whether it’s the major labels upset by its multi-million dollar lobbying of the CRB, or individual songwriters miffed at meagre royalty cheques, the service doesn’t have the best reputation amongst rights-holders big and small.

Yet Pandora needs the music industry’s support now more than ever.

A number of times in last night’s call with investors, both Pandora execs parroted a new company tagline: ‘We’ll provide music where you want it, how you want it and for everyone who wants it.’

McAndrews further summed up the company’s pitch to launch a multi-tiered subscription offering in future:

“The music industry’s brightest future lies in the monetising the entire spectrum of music listening; from ad-supported internet radio to full on-demand paid subscription.

“Nobody has the assets to monetise music like Pandora. We are the clear leader in ad-supported internet radio with massive scale. We are also the only streaming music company with a proven monetisation engine.

“This will be a huge advantage as we introduce and monetise new parts of the listening experience. It is notable that the more than $1.5bn in royalties we’ve paid came from converting listeners from broadcast radio to our superior listening experience, which pays significantly more in royalties to the music industry.

“As we look ahead we see the opportunity to match our audience with an offering that best suits their needs, and optimises the average revenue per user of all music consumers.”

To achieve that, Pandora needs fast-moving global expansion – and that means its needs its current publisher and label charm offensive to work.

“NOTHING’S GUARANTEED, BUT WE’RE HAVING THE RIGHT CONVERSATIONS.”

Through a historical failure to agree licenses with the likes of PRS and other rightsholder reps around the world, Pandora remains largely a US-only proposition – with some small market presence in Australia and New Zealand.

The fall-out from these royalty disagreements has coloured some music biz leaders’ views of Pandora, attitudes which have essentially blocked its plans to expand into other territories to date.

But, says Herring, that’s all changing…

“Even as recently as this last quarter, we’ve made significant steps in that direction,” he said. “For instance the pre-1972 agreement [where Pandora paid out a $90m settlement to the major labels and ABKCO] and our multi-year agreement with Sony/ATV… putting the CRB [lobbying] process behind us was also a big step.

“Nothing’s guaranteed, but we’re having the right conversations. We think we have an extremely valuable proposition to make to both labels and publishers and we look forward to working together with them to bring product to market that serves us well, serves the labels well, serves the publishers well and serves the listeners well.

“We’re optimistic we can make it happen, but there’s work to be done.”

McAndrews acknowledges a singular goal for his business: for Pandora to “become the definitive source for music enjoyment and discovery globally“.

It will be entertaining to see whether Pandora can convince rights-holders to sign new, worldwide licensing agreements with one of the most contentious streaming services in the world.

If it can’t, McAndrews’ grand global plan is dead in the water.

If it can, Pandora immediately becomes a very serious global player in the battle for streaming supremacy alongside Spotify, Apple Music and Google Play.

Pandora’s unique advantage? It’s the only streaming player with an owned live ticketing and promotion arm, and an ad-funded non-interactive business which truly rivals the commercial clout of commercial radio.

“We have only scratched the surface of the radio opportunity, both in the US and globally,” added McAndrews – a signal that Pandora’s intention to grow its current core business isn’t going anywhere.

“As a medium, radio enjoys 240m listeners weekly in the US alone and billions globally. Increased smartphone penetration, embedded connectivity in cars and the expansion of the internet of things will continue to drive the shift from broadcast and terrestrial radio to personalised and digital forms – and Pandora will continue driving this evolution.”

A final point: if Pandora wanted to increase it global subscriber footprint quickly, it may look to acquire again. From this angle, TIDAL, Deezer and Rhapsody/Napster all look like potentially juicy targets…